Abstract

Mental health conditions impose a substantial economic burden in India, yet evidence on treatment costs and insurance pricing-particularly for outpatient psychiatric care-remains limited. This cross-sectional study estimates provider-reported outpatient treatment costs for common and severe mental illnesses and derives indicative insurance premiums using a prevalence-based actuarial approach. Primary data were collected through structured interviews with 100 mental health professionals, including psychiatrists (n = 47), psychologists (n = 28), and counselors (n = 25), practicing in private outpatient clinics across four major referral hubs-Kolkata, New Delhi, Bangalore, and Pune. While 77% of clinics were urban and 23% semi-urban, providers served patients from urban, semi-urban, and rural areas. From the provider perspective, the estimated annual treatment cost for common mental illnesses such as depression and anxiety were INR 57,571, with psychological and pharmacological interventions accounting for 80.5% of out-of-pocket expenditure. For severe mental illnesses, including schizophrenia and bipolar disorder, the annual cost was higher at INR 77,237, largely driven by counseling, psychotherapy, and medication costs (85.4%). Based on prevalence-adjusted costing, pure risk premiums were estimated at INR 1,900 annually for depression and anxiety, INR 463 for bipolar disorder, and INR 232 for schizophrenia. Applying premium loadings of 40–90% to account for administrative costs and uncertainty yielded indicative insurance premiums aligned with early-stage mental health coverage markets. Although the estimates assume full treatment-seeking behavior and may overstate realized claims, they provide a pragmatic economic basis for mental health insurance pricing and policy planning in India.

Keywords

Mental Healthcare Act 2017, Health Insurance, Premium, Mental Disorders, Cost Estimation

1. Introduction

Mental disorders constitute a growing public health and economic challenge globally and in India. Between 1990 and 2019, DALYs attributable to mental disorders increased from 80.8 million to 125.3 million worldwide

| [1] | GBD 2019 Mental Disorders Collaborators (2022). Global, regional, and national burden of 12 mental disorders in 204 countries and territories, 1990-2019: a systematic analysis for the Global Burden of Disease Study 2019. The lancet. Psychiatry, 9(2), 137–150.

https://doi.org/10.1016/S2215-0366(21)00395-3 |

[1]

, with depressive and anxiety disorders contributing the largest share. In 2019, mental disorders ranked seventh among global causes of DALYs, while depression and anxiety were among the leading causes of YLDs

| [2] | Prakash, S., & India State-Level Disease Burden Initiative Collaborators. (2019). First comprehensive estimates of disease burden due to mental disorders and their trends in every state of India. Public Health Foundation of India. |

[2]

. These trends underscore the substantial productivity loss and long-term economic burden associated with mental illness.

In India, the burden of mental disorders has increased markedly over the past three decades. The India State-Level Disease Burden Initiative reported that the share of DALYs due to mental disorders nearly doubled from 2.5% in 1990 to 4.7% in 2017, affecting an estimated 197.3 million individuals

| [1] | GBD 2019 Mental Disorders Collaborators (2022). Global, regional, and national burden of 12 mental disorders in 204 countries and territories, 1990-2019: a systematic analysis for the Global Burden of Disease Study 2019. The lancet. Psychiatry, 9(2), 137–150.

https://doi.org/10.1016/S2215-0366(21)00395-3 |

| [2] | Prakash, S., & India State-Level Disease Burden Initiative Collaborators. (2019). First comprehensive estimates of disease burden due to mental disorders and their trends in every state of India. Public Health Foundation of India. |

[1, 2]

. Depression and anxiety alone accounted for nearly 90 million cases, while schizophrenia and bipolar disorder were among the leading contributors to YLDs

| [3] | Gururaj, G., Varghese, M., Benegal, V., Rao, G. N., Pathak, K., Singh, L. K., Mehta, R. Y., Ram, D., Shibukumar, T. M., Kokane, A., Lenin Singh, R. K., Chavan, B. S., Sharma, P., Ramasubramanian, C., Dalal, P. K., Saha, P. K., Deuri, S. P., Giri, A. K., Kavishvar, A. B., NMHS Collaborators Group. (2016). National Mental Health Survey of India, 2015–16: Summary (NIMHANS Publication No. 128). National Institute of Mental Health and Neuro Sciences. |

[3]

. Evidence from the National Mental Health Survey (2015–16)

| [3] | Gururaj, G., Varghese, M., Benegal, V., Rao, G. N., Pathak, K., Singh, L. K., Mehta, R. Y., Ram, D., Shibukumar, T. M., Kokane, A., Lenin Singh, R. K., Chavan, B. S., Sharma, P., Ramasubramanian, C., Dalal, P. K., Saha, P. K., Deuri, S. P., Giri, A. K., Kavishvar, A. B., NMHS Collaborators Group. (2016). National Mental Health Survey of India, 2015–16: Summary (NIMHANS Publication No. 128). National Institute of Mental Health and Neuro Sciences. |

[3]

suggests that common mental disorders affect nearly 10% of the adult population, with higher prevalence observed in urban and metropolitan areas.

Despite the high burden, India faces a substantial treatment gap, ranging from 70% to 92% across mental disorders

| [3] | Gururaj, G., Varghese, M., Benegal, V., Rao, G. N., Pathak, K., Singh, L. K., Mehta, R. Y., Ram, D., Shibukumar, T. M., Kokane, A., Lenin Singh, R. K., Chavan, B. S., Sharma, P., Ramasubramanian, C., Dalal, P. K., Saha, P. K., Deuri, S. P., Giri, A. K., Kavishvar, A. B., NMHS Collaborators Group. (2016). National Mental Health Survey of India, 2015–16: Summary (NIMHANS Publication No. 128). National Institute of Mental Health and Neuro Sciences. |

[3]

. This gap is driven by multiple factors, including shortages of trained mental health professionals, inadequate infrastructure, stigma, low awareness, and high OOP expenditures for long-term outpatient care. Limited financial protection further exacerbates access barriers. Historically, health insurance schemes in India have excluded psychiatric conditions, forcing households to bear treatment costs largely through OOP payments

.

The enactment of the MHCA, 2017

marked a policy shift by mandating parity between mental and physical health coverage. However, implementation remains inconsistent, and empirical evidence to guide mental health insurance design-particularly for outpatient care-is scarce

| [6] | Avula, V. C. R. (2025). Mental health insurance in India: An examination of policy implementation post-MHCA 2017. Indian Journal of Psychological Medicine. Advance online publication. https://doi.org/10.1177/02537176241236019 |

[6]

. Existing cost-of-illness studies in India have largely focused on tertiary care settings or small patient samples, often emphasizing indirect costs. There is limited provider-level evidence on routine outpatient treatment costs for common and severe mental disorders, which is critical for actuarial pricing and insurance product development.

Knowledge gap: There is a lack of empirically grounded estimates of outpatient mental health treatment costs in private settings in India and an absence of actuarial translation of these costs into insurance premiums.

Study objective: This study addresses this gap by estimating provider-reported outpatient treatment costs for common (depression, anxiety) and severe (schizophrenia, bipolar disorder) mental illnesses across major Indian cities and deriving prevalence-based pure risk premiums to inform mental health insurance pricing.

2. International Mental Health Insurance Plans

Mental health policies vary among developed countries, but most have policies in place to provide access to mental health services and support for individuals with mental health conditions. In developed countries, mental health insurance plans are typically provided as part of a comprehensive health insurance package. These plans vary in the type and amount of coverage they provide, but most aim to ensure that individuals have access to mental health services, such as therapy and medication.

Table 1. Mental Health insurance plans in developed countries.

Country | Mental Health Insurance Coverage |

United States | Mental health coverage is mandated under the Affordable Care Act (ACA); included in most private plans, Medicare, and Medicaid 7]. |

Singapore | Initially limited (AIA’s Beyond Critical Care plan in 2019), now expanding with more insurers offering custom plans and mental health riders 8]. |

Australia | Covered by both private insurance and the public Medicare scheme; up to 10 expert appointments/year, includes tele-consultation; 2-month wait period even for pre-existing conditions 9]. |

United Kingdom | Comprehensive mental healthcare provided free at point of care by the NHS (publicly funded system) 0]. |

China | Mental health disorders are covered under UEBMI (Urban Employee), URBMI (Urban Resident) NCMS (Rural) and private 1].China’s “686” program provides free medication and community-based mental health services for people with severe mental disorders, especially in urban areas 2].Private insurance is still nascent, covering only about 7% of the population and mainly targeting high-income households 2]. |

Austria | Public health scheme reimburses a significant portion of mental health costs; covers up to 40 appointments/year 3].For example, public health insurance (such as ÖGK) usually reimburses up to €28 per session with approved therapists, while patients pay the remaining amount out-of-pocket. Private therapy fees typically start at €75 per session 3].Private health insurance offers shorter wait times, longer or more frequent therapy sessions, and a broader choice of therapists and clinics compared to public insurance 3]. |

Switzerland | Both inpatient (hospital) and outpatient (clinic or private practice) psychiatric services are included in basic health insurance, provided they are deemed medically necessary and delivered by recognized providers 4].For broader coverage-such as more psychotherapy sessions, access to private mental health clinics, or alternative therapies-residents can purchase supplementary private insurance 4]. |

New Zealand | Most mental health services in New Zealand are funded by the government through Health New Zealand 5].About one-third of New Zealanders have private health insurance, mainly to access non-urgent or specialist services more quickly 5].Some plans offer up to NZD 2,500 per year for psychologist or psychiatrist consultations, with 100% reimbursement up to the cover limit, often requiring a GP referral 5]. |

3. Methods

3.1. Study Design and Data Collection

This study employed a cross-sectional design based on primary data collected from mental health professionals practicing in private outpatient psychiatric clinics across four major Indian cities-Kolkata, New Delhi, Bangalore, and Pune. Data were collected between March 2021 and August 2022. Due to COVID-19–related restrictions, data from Bangalore and New Delhi were obtained through online questionnaires (Google Forms), email, and telephonic interviews, while in-person interviews were conducted in Kolkata and Pune.

3.2. Questionnaire Development and Structure

Primary data were collected using a structured questionnaire designed to capture provider-reported outpatient treatment costs for common mental illnesses (depression and anxiety) and severe mental illnesses (schizophrenia and bipolar disorder). The questionnaire was developed following a review of relevant literature and consultations with subject experts to ensure relevance and completeness. Most items were closed-ended with numeric responses (e.g., cost per visit, number of sessions per year, medication costs), supplemented by a limited number of open-ended questions to capture context-specific variations in clinical practice.

3.3. Validity Assessment

Face and content validity of the questionnaire were assessed by three psychiatrists, including one senior research fellow. Face validity evaluated the clarity and appropriateness of the items, while content validity ensured comprehensive coverage of relevant treatment cost components. Feedback from the experts was incorporated into the final questionnaire. Formal psychometric reliability testing was not conducted, as the instrument captured factual cost information rather than latent constructs.

3.4. Treatment Protocols

Table 2. Treatment Protocol.

Disorders | Minimum No. of Counseling Sessions | Minimum No. of Psychotherapy Sessions | Minimum Duration of Treatment |

Depression | 6-8 | 6-8 | 6-9 months |

Anxiety | 6-8 | 6-8 | 9-12 months |

Schizophrenia | 8-12 | 10-15 | 12-24 months (follow-up lifetime) |

Bipolar Disorder | 8-12 | 10-15 | 12-24 months (follow-up lifetime) |

During provider interviews, clinicians were asked to report typical treatment patterns followed in their outpatient practice. These reported practices were mapped against NICE-recommended treatment pathways to standardize cost components and avoid extreme variability across providers.

3.5. Cost

Cost-related data were collected through structured interviews with 100 mental health professionals (psychiatrists, psychologists, and counselors) practicing in private outpatient clinics across Kolkata, New Delhi, Bangalore, and Pune. For each disorder category, costs were calculated by aggregating the reported expenses associated with outpatient consultations, medications, psychotherapy or counseling sessions, investigations, and follow-up visits over one year. The non-medical direct expenses such as transportation, accommodation (if any), food, property losses, care giver’s income are not included in the study.

3.6. Analysis of Data

Provider-reported cost data were compiled and processed at the individual respondent level. For each treatment component (consultations, medications, psychotherapy/counseling, investigations, and follow-up visits), mean annual costs were calculated across all respondents. The primary results are reported as average (mean) costs, as these values are required for prevalence-based cost estimation and actuarial premium calculations. Measures of dispersion, including standard deviations, were calculated during data validation to assess variability and identify extreme values. Microsoft excel was utilized for this tabulation, employing necessary tools whenever applicable.

Table 3. Descriptive Statistics.

Descriptive Statistics | Consultation Fees | Follow up Fees | Counseling cost per session | Psychotherapy cost per session | Medicinal Costs | Miscellaneous Costs |

Mean | 1259 | 1010 | 1470 | 1974 | 1562 | 5944 |

SD | 436 | 360 | 375 | 457 | 457 | 1529 |

3.7. Calculation of Premium - Pure Risk Premium

The pure premium, also known as the risk premium, primarily consists of the combined impact of the frequency and average cost for each risk group or insured individual and the chosen coverage. Premium modeling involves calculating these effects separately and then multiplying them, which requires detailed information on these variables. Alternatively, premium modeling can be done using data on claims and exposure to determine the pure premium. The pure premium aims to represent the amount per exposure needed to collect sufficient funds to cover anticipated claims. While determining the appropriate exposure variable is beyond the scope of this discussion, it is important to note that calculating premiums in monetary terms is the most common and straightforward approach. In this paper, we will use the simplest premium calculation principle known as the pure risk premium, which are applied to life and some non-life insurance models.

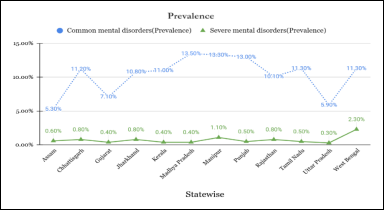

Figure 1. Prevalence of mental disorders in India.

Generally, the pure risk premium is calculated from:

Pure Risk Premium (PR) = Probability of occurrence of the event x Average cost of the occurrence

One reason for modeling the pure premium in monetary units or as a rate is how the severity varies with the insured sum. This involves determining whether the severity is constant across different insured sum ranges or if the severity rate remains constant. To arrive at the premium rate, it was important to understand the prevalence of mental disorder and its burden in India. According to the NMHS

| [3] | Gururaj, G., Varghese, M., Benegal, V., Rao, G. N., Pathak, K., Singh, L. K., Mehta, R. Y., Ram, D., Shibukumar, T. M., Kokane, A., Lenin Singh, R. K., Chavan, B. S., Sharma, P., Ramasubramanian, C., Dalal, P. K., Saha, P. K., Deuri, S. P., Giri, A. K., Kavishvar, A. B., NMHS Collaborators Group. (2016). National Mental Health Survey of India, 2015–16: Summary (NIMHANS Publication No. 128). National Institute of Mental Health and Neuro Sciences. |

[3]

, the crude prevalence rate of depressive disorder and anxiety disorders were 3.4% and 3.3% respectively and the prevalence rate of bipolar disorder and schizophrenia were 0.6% and 0.3% and the symptoms are more pronounced during adulthood.

4. Results

4.1. Cost of Illness

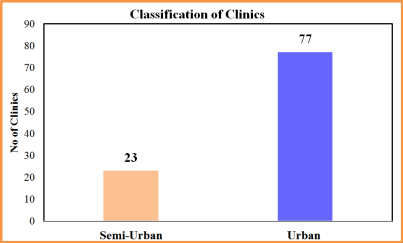

The study was conducted in private clinics of four mega cities of India namely Kolkata, New Delhi, Bangalore and Pune which provided outpatient psychiatric services. The patients are self-referred or referred by general physicians, friends or relatives. Though 77% of the data is collected from urban clinics and 23% are from semi urban respectively. While the study is based in these four metro cities- these were strategically chosen as they serve as major referral hubs for mental health care. Mental health facilities in these cities receive patients from a wide catchment area, including rural and semi-urban regions. As a result, the doctors interviewed cater to a diverse patient base, reflecting a broader mental health landscape beyond just urban populations.

Figure 2. Classification of clinics.

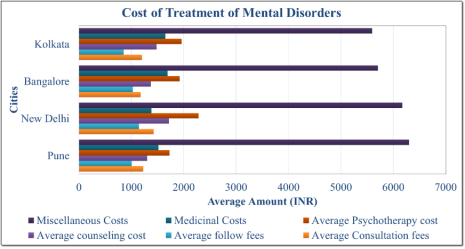

Figure 3. Costs across 4 Mega cities.

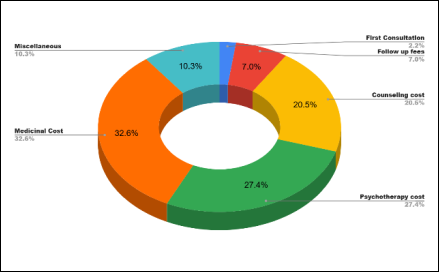

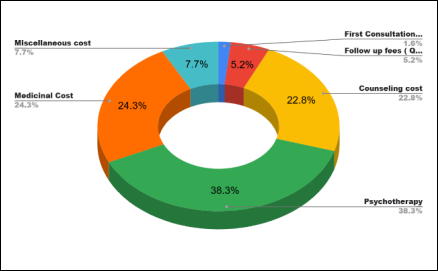

Figure 4. Cost of Mental Illness (Common Mental Disorders).

Figure 5. Cost of Mental Illness (Severe Mental Disorders).

The above figure provides information about the costs associated with the treatment of common and severe mental health disorders in India. From the table, it is clear that the cost of mental health treatment can vary depending on the type and severity of the disorder. For individuals with common mental illnesses such as depression and anxiety, the total cost of treatment is estimated to be Rs. 57,571 per year. 80.5% of the OOP expenditure is spend on the psychological and pharmacological interventions. For individuals with more severe disorders such as bipolar disorder and schizophrenia, the total cost of treatment is higher, at Rs. 77,237 per year. 85.4% of the expenses are incurred due to increased cost of counseling and psychotherapy sessions, as well as the cost of medications.

4.2. Pure Risk Premium

In this study, the pure risk premium for common and severe mental disorders was estimated using a prevalence-based costing approach. By multiplying the annual cost of treatment with the population prevalence rates, we derived average expected costs per individual in the insured population. For example, the pure premium for depression and anxiety was calculated at INR1,900 annually, while for bipolar disorder and schizophrenia, it was INR463 and INR232, respectively. This method aligns with standard actuarial practices and provides a realistic foundation for mental health insurance pricing in India. However, it assumes full treatment-seeking behavior and may overestimate actual claims, given existing barriers like stigma and limited access to care.

Table 4. Pure Risk premium calculation.

Disorders | Depression | Anxiety | Bipolar Disorder | Schizophrenia |

Prevalence Rate* | 3.30% | 3.30% | 0.60% | 0.30% |

Yearly cost of treatment | 57571 | 57571 | 77237 | 77237 |

Pure risk premium (Yearly) | 1900 | 1900 | 463 | 232 |

Premium loading refers to the additional amount charged by insurers over and above the pure risk premium to account for administrative costs, reserves, profit margins, and potential uncertainties in claims. In the context of mental health insurance, higher loadings are often applied due to data limitations, underreporting of illness, and uncertainty around treatment-seeking behavior, especially in outpatient settings. For this study, various loading margins (40%, 50%, 70%, and 90%) were applied to the calculated pure risk premiums to estimate indicative annual premiums. For example, with a 50% loading, a pure premium of INR1,900 for depression or anxiety would translate into a final premium of INR2,850 per year. These loadings help insurers remain financially viable while accommodating risks associated with early-stage implementation of mental health coverage in India. However, as better data emerges and utilization stabilizes, lower and more predictable loadings may become feasible.

Formula for Premium Loading = Pure Risk Premium × (1 + Margin %)

Table 5. A premium loading.

Disorder | Pure Risk Premium (INR) | 40% Margin (INR) | 50% Margin (INR) | 70% Margin (INR) | 90% Margin (INR) |

Depression | 1,900 | 2,660 | 2,850 | 3,230 | 3,610 |

Anxiety | 1,900 | 2,660 | 2,850 | 3,230 | 3,610 |

Bipolar Disorder | 463 | 648 | 695 | 787 | 880 |

Schizophrenia | 232 | 325 | 348 | 394 | 441 |

5. Discussion

In India, a large portion of healthcare expenses-around 40%-is paid directly by individuals from their own pockets, according to earlier studies. This heavy financial burden often becomes a serious hurdle, especially when it comes to seeking mental health care. For those diagnosed with common or severe mental disorders, the annual cost of treatment can range between INR 57,500 and INR 77,200 per person. These figures are in line with more recent findings-for instance, a 2022 study conducted in an academic tertiary care hospital estimated the average treatment cost at INR 62,676 per patient

| [17] | Kondapura, M. B., Manjunatha, N., Nagaraj, A. K. M., Praharaj, S. K., Kumar, C. N., Math, S. B., & Rao, G. N. (2023). Cost of illness analysis of common mental disorders: A study from an Indian academic tertiary care hospital. Indian Journal of Psychological Medicine, 45(5), 519–525.

https://doi.org/10.1177/02537176221108867 |

[17]

. When compared these expenses to India's per capita income of INR 1,72,000 (2022–23, as per NSO data), it becomes clear that the cost of mental healthcare remains quite substantial for most families.

According to a study conducted in India in 2012 suggested that the expense of mental health treatments and services in India includes both direct and indirect costs

. The direct costs encompass diagnostic and therapeutic costs, as well as other costs such as travel and living expenses. Indirect costs include the lost income of caregivers, a low level of education, and the burden of DALYs from comorbidities. In another study conducted it was found that the median monetary cost of the pathway to psychiatric care in Jaipur, India, was INR 3565

| [19] | Jain, N., Singh, H., & Pathak, A. (2013). Pathway to psychiatric care in a tertiary mental health centre in North India. Asian Journal of Psychiatry, 6(1), 39–43.

https://doi.org/10.1016/j.ajp.2012.09.004 |

[19]

. In another study of 140 patients, it was found that the average monthly total cost of treatment of INR 770

. For bipolar illness, the total monthly treatment costs were INR 750; for schizophrenia, they were INR 720; and for nonspecific nonorganic psychosis, they were INR 830

. The study estimated that the cost of bipolar disorder was somewhat higher than the price of schizophrenia in a tertiary care general hospital in Delhi providing free medical facilities. The mean cost per psychiatric outpatient visit in Chattisgarh in India was INR 2643 for services from formal for-profit providers, INR 586 for informal private providers, and INR 400 for public services

| [22] | Garg, S., & Singh, R. (2021). Comparing the average cost of outpatient care of public and for-profit private providers in India. Health Policy and Planning, 36(7), 1122–1133.

https://doi.org/10.1093/heapol/czab064 |

[22]

. Similar kind of study estimated the annual outpatient cost of 50 schizophrenic patients in India was US$274

| [23] | Grover, S., Avasthi, A., Chakrabarti, S., Bhargava, V., Sharan, P., Kumar, S., & Singh, A. (2005). Cost of care of schizophrenia: A study of Indian out-patient attenders. Acta Psychiatrica Scandinavica, 112(4), 279–285.

https://doi.org/10.1111/j.1600-0447.2005.00579.x |

[23]

; however, due to the higher indirect costs associated with mental disorders

, however it is challenging to accurately estimate the true economic burden of sickness.

The findings of this study highlight the substantial outpatient cost burden associated with both common and severe mental disorders in India. A large share of expenditure is driven by recurring costs related to consultations, pharmacological treatment, and psychotherapy, underscoring the chronic and resource-intensive nature of mental health care. Many mental disorders have their onset in adolescence or early adulthood, and evidence suggests that early intervention leads to better long-term clinical and economic outcomes

. This presents an opportunity to develop age-sensitive mental health insurance products with lower premiums that encourage early enrolment and strengthen risk pooling. However, uncertainty in disease trajectories, reliance on long-term outpatient care, and underutilization driven by stigma complicate risk estimation and claims predictability. Consequently, insurers may initially apply higher premium loadings to manage uncertainty. As utilization increases and more representative claims data become available, improved risk adjustment models may enable more accurate pricing and enhanced affordability. While this study focuses on outpatient costs, which constitute the majority of ongoing mental health expenditure, the absence of inpatient cost data remains a limitation.

6. The Way Forward

This study generates indicative estimates of pure risk premiums for common and severe mental disorders in India, contributing evidence for the design of mental health insurance products. Given the predominantly outpatient and long-term nature of mental healthcare, insurance models restricted to inpatient coverage are insufficient to provide effective financial risk protection. Integrating outpatient and inpatient services within comprehensive health insurance plans-preferably as add-on benefits-may enhance affordability, utilization, and sustainability.

However, premium estimation remains constrained by limited prevalence, utilization, and claims data. The cross-sectional design, provider-reported costs, and restricted geographic coverage limit generalizability. Future multicentric, longitudinal studies incorporating both outpatient and inpatient costs are essential to improve cost accuracy and support actuarially sound mental health insurance design as claims data mature.

Abbreviations

OOP | Out-of-pocket |

DALYs | Disability-Adjusted Life Years |

YLDs | Years Lived with Disability |

MHCA | Mental Healthcare Act |

Author Contributions

Madhurima Ghosh is the sole author. The author read and approved the final manuscript.

Conflicts of Interest

The author declares no conflicts of interest.

References

| [1] |

GBD 2019 Mental Disorders Collaborators (2022). Global, regional, and national burden of 12 mental disorders in 204 countries and territories, 1990-2019: a systematic analysis for the Global Burden of Disease Study 2019. The lancet. Psychiatry, 9(2), 137–150.

https://doi.org/10.1016/S2215-0366(21)00395-3

|

| [2] |

Prakash, S., & India State-Level Disease Burden Initiative Collaborators. (2019). First comprehensive estimates of disease burden due to mental disorders and their trends in every state of India. Public Health Foundation of India.

|

| [3] |

Gururaj, G., Varghese, M., Benegal, V., Rao, G. N., Pathak, K., Singh, L. K., Mehta, R. Y., Ram, D., Shibukumar, T. M., Kokane, A., Lenin Singh, R. K., Chavan, B. S., Sharma, P., Ramasubramanian, C., Dalal, P. K., Saha, P. K., Deuri, S. P., Giri, A. K., Kavishvar, A. B., NMHS Collaborators Group. (2016). National Mental Health Survey of India, 2015–16: Summary (NIMHANS Publication No. 128). National Institute of Mental Health and Neuro Sciences.

|

| [4] |

Kapoor, V., & Mahashur, A. (2021, June 18). Right to health insurance: Ensuring parity for mental illness in India. JURIST.

https://www.jurist.org/commentary/2021/06/kapoor-mahashur-health-insurance-india/

|

| [5] |

Government of India. (2017). The Mental Healthcare Act, 2017 (No. 10 of 2017). Ministry of Law and Justice, Gazette ofIndia.

https://www.indiacode.nic.in/bitstream/123456789/2249/1/A2017-10.pdf

|

| [6] |

Avula, V. C. R. (2025). Mental health insurance in India: An examination of policy implementation post-MHCA 2017. Indian Journal of Psychological Medicine. Advance online publication.

https://doi.org/10.1177/02537176241236019

|

| [7] |

Breslau, J., Yu, M., Collins, R. L., Tanielian, T., Malsberger, R., & Kataoka, S. H. (2020). Impact of the ACA Medicaid expansion on utilization of mental health care. Medical Care, 58(9), 757–764.

https://doi.org/10.1097/MLR.0000000000001348

|

| [8] |

AIA Singapore. (n.d.). AIA Beyond Critical Care.

https://www.aia.com.sg/en/our-products/health/critical-illness/aia-beyond-critical-care.html

|

| [9] |

Australian Government Department of Health. (2023, April 26). Waiting periods and exemptions.

https://www.health.gov.au/topics/private-health-insurance/what-private-health-insurance-covers/waiting-periods-and-exemptions

|

| [10] |

Thorlby, R. (2020). England | International Health Care System Profiles. The Commonwealth Fund.

https://www.commonwealthfund.org/international-health-policy-center/countries/england

|

| [11] |

Liu, J., Ma, H., He, Y. L., Xie, B., Xu, Y. F., Tang, H. Y., Li, M., Hao, W., Wang, X. D., Zhang, M. Y., & Ng, C. H. (2011). Mental health system in China: History, recent service reform and future challenges. World Psychiatry, 10(3), 210–216.

|

| [12] |

Xu, J., Wang, J., Wimo, A., Qiu, C., & Fratiglioni, L. (2018). Rural–urban disparities in the utilization of mental health inpatient services in China: The role of health insurance. International Journal of Environmental Research and Public Health, 15(3), 479.

|

| [13] |

Expatica. (2025, August 26). Accessing mental health services in Austria.

https://www.expatica.com/at/healthcare/healthcare-services/austria-mental-health-109300/

|

| [14] |

Stulz, N., Jörg, R., Reim-Gautier, C., Bonsack, C., Conus, P., Evans-Lacko, S., Gabriel-Felleiter, K., Heim, E., Jäger, M., Knapp, M., Richter, D., Schneeberger, A., Thornicroft, G., Traber, R., Wieser, S., Tuch, A., & Hepp, U. (2023). Mental health service areas in Switzerland. International Journal of Methods in Psychiatric Research, 32(1), e1937.

https://doi.org/10.1002/mpr.1937

|

| [15] |

Ramalho, R., McKenna, B., Adams, C., & Smith, M. (2023). Community mental health care in Aotearoa New Zealand: Reflections on the COVID-19 pandemic. International Journal of Mental Health Nursing, 32(1), 4–12.

https://doi.org/10.1111/inm.13055

|

| [16] |

National Institute for Health and Care Excellence. (2022).

https://www.nice.org.uk/guidance

|

| [17] |

Kondapura, M. B., Manjunatha, N., Nagaraj, A. K. M., Praharaj, S. K., Kumar, C. N., Math, S. B., & Rao, G. N. (2023). Cost of illness analysis of common mental disorders: A study from an Indian academic tertiary care hospital. Indian Journal of Psychological Medicine, 45(5), 519–525.

https://doi.org/10.1177/02537176221108867

|

| [18] |

Yerramilli, S. S. R. R., & Bipeta, R. (2012). Economics of mental health: Part I - Economic consequences of neglecting mental health - an Indian perspective. AP Journal of Psychological Medicine, 13(2), 80–86.

https://mhi.org.in/media/insight_files/aagt12i2p80.pdf

|

| [19] |

Jain, N., Singh, H., & Pathak, A. (2013). Pathway to psychiatric care in a tertiary mental health centre in North India. Asian Journal of Psychiatry, 6(1), 39–43.

https://doi.org/10.1016/j.ajp.2012.09.004

|

| [20] |

Sarkar, D., & Chandra, S. (2017). Cost-of-treatment of clinically stable severe mental illnesses in India: Analysis of published data. Journal of Clinical and Scientific Research, 6(2), 96–100.

https://doaj.org/article/d3fe893d161f4951958e148ddfafbcb2

|

| [21] |

Sharma, V., Das, S., & Grover, S. (2004). An estimate of the monthly cost of two major mental disorders in an Indian metropolis. Indian Journal of Psychiatry, 46(4), 289–295.

https://pmc.ncbi.nlm.nih.gov/articles/PMC2932983/

|

| [22] |

Garg, S., & Singh, R. (2021). Comparing the average cost of outpatient care of public and for-profit private providers in India. Health Policy and Planning, 36(7), 1122–1133.

https://doi.org/10.1093/heapol/czab064

|

| [23] |

Grover, S., Avasthi, A., Chakrabarti, S., Bhargava, V., Sharan, P., Kumar, S., & Singh, A. (2005). Cost of care of schizophrenia: A study of Indian out-patient attenders. Acta Psychiatrica Scandinavica, 112(4), 279–285.

https://doi.org/10.1111/j.1600-0447.2005.00579.x

|

| [24] |

McGorry, P. D., & Mei, C. (2018). Early intervention in youth mental health: progress and future directions. Evidence-Based Mental Health, 21(4), 182–184.

https://doi.org/10.1136/ebmental-2018-300060

|

Cite This Article

-

-

@article{10.11648/j.ijebo.20261401.11,

author = {Madhurima Ghosh},

title = {Modeling Pure Risk Premium for Mental Health Insurance in India: An Actuarial Approach},

journal = {International Journal of Economic Behavior and Organization},

volume = {14},

number = {1},

pages = {1-9},

doi = {10.11648/j.ijebo.20261401.11},

url = {https://doi.org/10.11648/j.ijebo.20261401.11},

eprint = {https://article.sciencepublishinggroup.com/pdf/10.11648.j.ijebo.20261401.11},

abstract = {Mental health conditions impose a substantial economic burden in India, yet evidence on treatment costs and insurance pricing-particularly for outpatient psychiatric care-remains limited. This cross-sectional study estimates provider-reported outpatient treatment costs for common and severe mental illnesses and derives indicative insurance premiums using a prevalence-based actuarial approach. Primary data were collected through structured interviews with 100 mental health professionals, including psychiatrists (n = 47), psychologists (n = 28), and counselors (n = 25), practicing in private outpatient clinics across four major referral hubs-Kolkata, New Delhi, Bangalore, and Pune. While 77% of clinics were urban and 23% semi-urban, providers served patients from urban, semi-urban, and rural areas. From the provider perspective, the estimated annual treatment cost for common mental illnesses such as depression and anxiety were INR 57,571, with psychological and pharmacological interventions accounting for 80.5% of out-of-pocket expenditure. For severe mental illnesses, including schizophrenia and bipolar disorder, the annual cost was higher at INR 77,237, largely driven by counseling, psychotherapy, and medication costs (85.4%). Based on prevalence-adjusted costing, pure risk premiums were estimated at INR 1,900 annually for depression and anxiety, INR 463 for bipolar disorder, and INR 232 for schizophrenia. Applying premium loadings of 40–90% to account for administrative costs and uncertainty yielded indicative insurance premiums aligned with early-stage mental health coverage markets. Although the estimates assume full treatment-seeking behavior and may overstate realized claims, they provide a pragmatic economic basis for mental health insurance pricing and policy planning in India.},

year = {2026}

}

Copy

|

Copy

|

Download

Download

-

TY - JOUR

T1 - Modeling Pure Risk Premium for Mental Health Insurance in India: An Actuarial Approach

AU - Madhurima Ghosh

Y1 - 2026/02/02

PY - 2026

N1 - https://doi.org/10.11648/j.ijebo.20261401.11

DO - 10.11648/j.ijebo.20261401.11

T2 - International Journal of Economic Behavior and Organization

JF - International Journal of Economic Behavior and Organization

JO - International Journal of Economic Behavior and Organization

SP - 1

EP - 9

PB - Science Publishing Group

SN - 2328-7616

UR - https://doi.org/10.11648/j.ijebo.20261401.11

AB - Mental health conditions impose a substantial economic burden in India, yet evidence on treatment costs and insurance pricing-particularly for outpatient psychiatric care-remains limited. This cross-sectional study estimates provider-reported outpatient treatment costs for common and severe mental illnesses and derives indicative insurance premiums using a prevalence-based actuarial approach. Primary data were collected through structured interviews with 100 mental health professionals, including psychiatrists (n = 47), psychologists (n = 28), and counselors (n = 25), practicing in private outpatient clinics across four major referral hubs-Kolkata, New Delhi, Bangalore, and Pune. While 77% of clinics were urban and 23% semi-urban, providers served patients from urban, semi-urban, and rural areas. From the provider perspective, the estimated annual treatment cost for common mental illnesses such as depression and anxiety were INR 57,571, with psychological and pharmacological interventions accounting for 80.5% of out-of-pocket expenditure. For severe mental illnesses, including schizophrenia and bipolar disorder, the annual cost was higher at INR 77,237, largely driven by counseling, psychotherapy, and medication costs (85.4%). Based on prevalence-adjusted costing, pure risk premiums were estimated at INR 1,900 annually for depression and anxiety, INR 463 for bipolar disorder, and INR 232 for schizophrenia. Applying premium loadings of 40–90% to account for administrative costs and uncertainty yielded indicative insurance premiums aligned with early-stage mental health coverage markets. Although the estimates assume full treatment-seeking behavior and may overstate realized claims, they provide a pragmatic economic basis for mental health insurance pricing and policy planning in India.

VL - 14

IS - 1

ER -

Copy

|

Download